Property Prices in Malta

These documents contain excerpts about property prices in Malta, mdina and valletta obtained from the Central Bank Annual Reports issued between 1998 and 2009. Excerpts taken from the Central Bank Annual Reports:

http://www.centralbankmalta.com/site/publications2.asp

To view a particular document click on one of the 'View Report' links below. You are also

able to download the respective documents by right-clicking on one of the 'Download Report' links and selecting 'Save Target As...'

View Report: [2009] [2008] [2007] [2006] [2005] [2004 - 2001] [2000 - 1998]

Download Report: [2009] [2008] [2007] [2006] [2005] [2004 - 2001] [2000 - 1998]

2007 Report

Construction

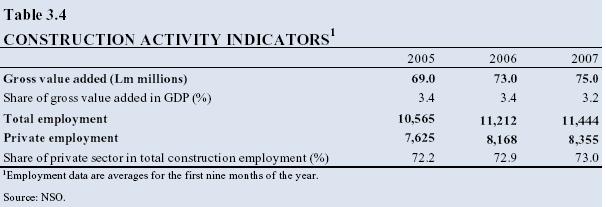

After having increased by 5.9% in 2006, the gross value added of the construction industry, measured

in nominal terms, rose by 2.7% in 2007 (see Table 3.4).

According to ETC data, full-time employment in

private construction increased by 2.3% during the

first nine months of 2007, as against 7.1% in 2006.

After having declined in 2006, the industry’s average

annual gross salary as reported in the LFS rose by

2.3% in the first three quarters of the year, a faster rate

than the 1.7% recorded across all other sectors.

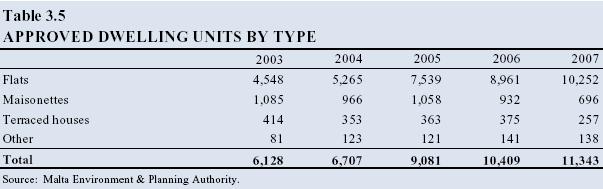

At the same time, there was a 9.0% rise in the number

of building permits issued during the year. Although

still high, the rate of increase was sharply down from

the double-digit growth rates of previous years. The

preponderance of permits issued in 2007 was for flats,

while approvals for other dwelling types declined from

the level of the year before (see Table 3.5).

Residential Property Prices

The rate of increase in residential property prices

decelerated further in 2007, to 1.1% (see Chart 3.5),

reflecting a slowdown in asked prices for most

property types, particularly flats. While prices for

finished flats, the predominant category, rose by 1.8%,

as against 2.5% a year earlier, those for flats in shell

form went up by 1.4%, considerably slower than the

8.5% rise recorded in 2006.

Similarly, growth in asked prices for villas decelerated

to 0.9%, from 10.6% in 2006. Prices for maisonettes in

finished form and town houses contracted by 4.6%

and 7.1%, respectively. On the other hand, prices of

terraced houses and houses of character increased

by 4.6% and 11.0%, respectively.

Financial Stability Analysis

In 2007 favourable domestic economic conditions

continued to sustain the financial sector’s positive

performance. The capital buffer of the banking sector

as a whole increased, complemented by an

improvement in asset quality, though profits remained

at the same level as in the previous year. The same

trends were reported by domestic banks, except for a

small decline in profits. At the same time, the financial

standing of households improved further, reflecting

the rise in compensation levels nationally and the fall

in the unemployment rate. The corporate sector

registered higher gearing and liquidity ratios and stable

profitability.

These developments also led to an

improvement in the quality of bank asset portfolios.

Nevertheless, the private sector continued to

accumulate debt which, in the case of an economic

downturn, could put some strain on repayment

capability and, hence, on the banks’ profits and capital

base. This would be more acute if – given the high

concentration of the banks’ exposures to real estate –

a sharp fall in property prices resulted in a rise in

borrowers’ default rates.

The non-financial Sector

The household sector

Household credit demand continued to be a major

stimulus for the growth in the banks’ lending portfolio,

although banks reported a slowdown in demand

towards the end of 2007, as indicated by the responses

to the Bank Lending Survey (BLS).9 The expansion in

credit demand was also reflected in household

indebtedness to banks, which continued to increase

throughout the year, reaching 58% of GDP, almost in

line with the euro area average. Although the resilience

of households to macroeconomic shocks improved,

helped by the further accumulation of wealth, the

increase in the debt-servicing ratio could result in more

debt-repayment problems in the future. The

proportion of household NPLs to total household

loans remained stable at 2.3%. However, the continued

strong growth in household debt during recent years

implies a build-up of risks. In fact, shocks to

disposable income and wealth remain the major source

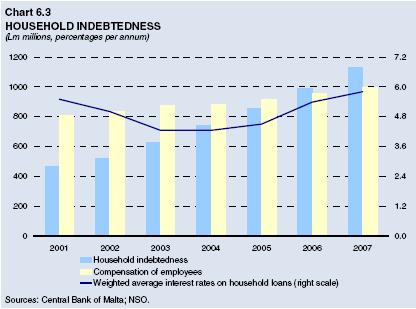

of vulnerability for households. As indicated in

Chart 6.3, household indebtedness continued to

increase, while compensation to employees increased

at a slower rate during 2007.

The Corporate Sector

A larger proportion of corporate financing needs was

met through the capital market during the year.

Nonetheless, borrowing from banks – which remained

the main source of external funding for firms –

continued to grow during the year, driven primarily

by real estate related loans. Risks associated with

such lending have grown as a result of cyclical and

structural factors. These include both an increase in

the mismatch between the supply and the demand for

property, and the high concentration of bank

exposures to this sector. Indeed, given that corporate

bond issuance during the year was related largely to

the construction industry, this disintermediation may

have partly resulted from tighter standards adopted

by credit institutions.

|